Imagine you walk into a store, pick up your favorite items, and head to the counter. You swipe your card, but what happens next depends on whether it’s credit or debit.

This everyday moment perfectly explains the difference between credit & debit two financial tools we use regularly but often misunderstand. Credit allows you to borrow money and pay later, while debit deducts money directly from your bank account instantly.

In today’s fast-moving world, knowing the difference between credit & debit is essential for managing finances wisely. If you’re shopping online, paying bills, or saving money, understanding the difference between credit & debit helps you avoid debt and make smarter decisions.

Many people confuse these terms, but learning the difference between credit & debit can improve both personal and professional financial habits.

Key Difference Between the Both

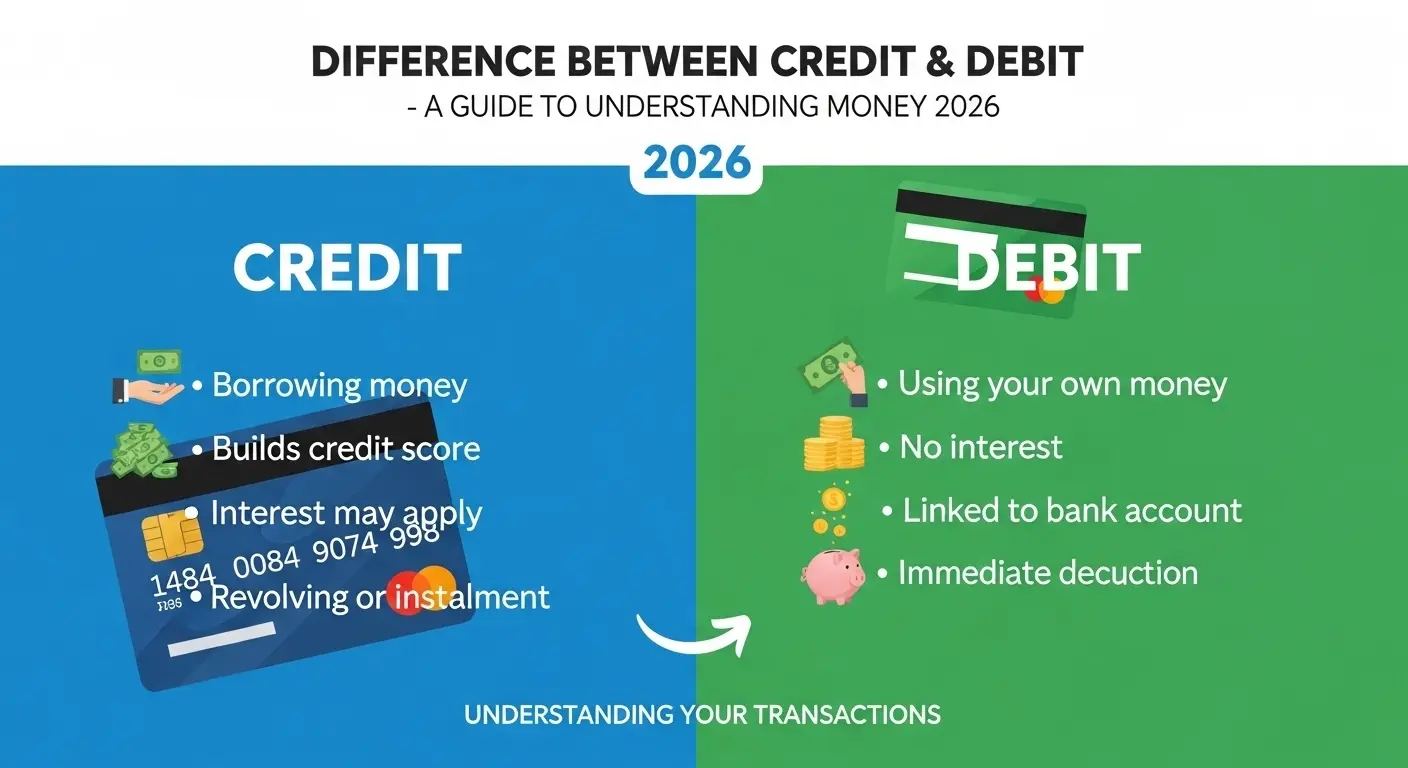

The main difference is simple:

- Credit means borrowing money to pay later.

- Debit means using your own money immediately.

Why Is Their Difference Necessary to Know?

Understanding the difference between credit & debit is important for both beginners and experts. For learners, it builds a strong financial foundation. For professionals, it helps in budgeting, investment decisions, and financial planning. In society, these tools shape spending behavior, influence credit scores, and determine financial stability.

Misusing credit can lead to debt, while improper debit usage may result in poor cash management. Knowing the distinction empowers individuals to make responsible financial choices and maintain economic balance.

Pronunciation (US & UK)

- Credit

- US: /ˈkrɛdɪt/

- UK: /ˈkrɛdɪt/

- Debit

- US: /ˈdɛbɪt/

- UK: /ˈdɛbɪt/

Difference Between Credit & Debit

1. Source of Money

- Credit: Borrowed from a bank

- Example 1: Using a credit card to buy a phone

- Example 2: Paying for a hotel stay with borrowed funds

- Debit: Comes from your bank account

- Example 1: Paying groceries with a debit card

- Example 2: ATM withdrawal

2. Payment Timing

- Credit: Pay later

- Example 1: Monthly credit card bill

- Example 2: EMI payments

- Debit: Pay instantly

- Example 1: Immediate deduction after purchase

- Example 2: Online bank transfer

3. Interest Charges

- Credit: Interest applies if unpaid

- Example 1: Late credit card payment

- Example 2: Carrying balance monthly

- Debit: No interest

- Example 1: Direct payment

- Example 2: Bank transfer

4. Spending Limit

- Credit: Pre-set limit

- Example 1: $2000 credit limit

- Example 2: Increased credit line

- Debit: Based on account balance

- Example 1: Limited by savings

- Example 2: Cannot exceed funds

5. Credit Score Impact

- Credit: Affects score

- Example 1: Timely payments improve score

- Example 2: Missed payments harm score

- Debit: No effect

- Example 1: Transactions not reported

- Example 2: No borrowing record

6. Risk Factor

- Credit: Risk of debt

- Example 1: Overspending

- Example 2: Accumulated interest

- Debit: Low risk

- Example 1: Spend only what you have

- Example 2: No borrowing

7. Rewards & Benefits

- Credit: Offers rewards

- Example 1: Cashback

- Example 2: Travel points

- Debit: Limited rewards

- Example 1: Basic cashback

- Example 2: Discounts

8. Fraud Protection

- Credit: Strong protection

- Example 1: Disputed charges

- Example 2: Refunds

- Debit: Less protection

- Example 1: Direct account loss

- Example 2: Slower recovery

9. Usage Purpose

- Credit: Big purchases

- Example 1: Electronics

- Example 2: Travel bookings

- Debit: Daily expenses

- Example 1: Food

- Example 2: Bills

10. Financial Discipline

- Credit: Requires control

- Example 1: Budget tracking

- Example 2: Timely repayment

- Debit: Promotes discipline

- Example 1: Limited spending

- Example 2: Savings habit

Nature and Behaviour

- Credit: Flexible, risky, and future-oriented. Encourages spending beyond current means but helps build financial history.

- Debit: Safe, controlled, and present-focused. Encourages spending within limits and supports budgeting.

Why People Are Confused

People often confuse credit and debit because both use cards, look similar, and are accepted in the same places. The transaction process feels identical, making it difficult to distinguish their financial impact.

Table: Difference and Similarity

| Feature | Credit | Debit | Similarity |

| Source | Borrowed money | Own money | Both used for payments |

| Timing | Pay later | Pay now | Accepted worldwide |

| Interest | Yes | No | Require card |

| Risk | High | Low | Used online/offline |

| Control | Needs discipline | Automatic control | Convenient |

Which Is Better in What Situation?

Credit is better when making large purchases or when you need flexibility. It is ideal for emergencies, travel, or building a credit score. However, it requires discipline to avoid debt and interest.

Debit is better for daily spending and budgeting. It ensures you only spend what you have, making it perfect for controlling expenses and avoiding financial stress.

Metaphors and Similes

- Credit is like borrowing tomorrow’s money today.

- Debit is like spending cash from your wallet.

Connotative Meanings

- Credit

- Positive: Opportunity, trust (e.g., “She has good credit”)

- Negative: Debt, burden (e.g., “He is trapped in credit”)

- Debit

- Neutral/Positive: Control, stability (e.g., “He uses debit wisely”)

- Slight Negative: Limitation (e.g., “Debit restricts spending”)

Idioms & Proverbs

- “Give credit where credit is due”

- Example: Always appreciate hard work.

- “In the red” (related to debit/account deficit)

- Example: The company is in the red this year.

Works in Literature

- Credit and Debt in Modern Society Economics, John Smith, 2010

- The Psychology of Spending Finance, Jane Doe, 2015

Movies Related to Keywords

- Inside Job (2010, USA)

- The Big Short (2015, USA)

FAQs:

1. What is the main difference between credit & debit?

Credit borrows money; debit uses your own money.

2. Does debit affect credit score?

No, only credit impacts your score.

3. Which is safer?

Debit is safer for spending control; credit offers better fraud protection.

4. Can I use both together?

Yes, many people use debit for daily expenses and credit for big purchases.

5. Which is better for beginners?

Debit is better for beginners due to lower risk.

How Both Are Useful for Surroundings

Credit supports economic growth by enabling purchases and investments, while debit ensures financial stability and responsible spending. Together, they balance the financial ecosystem.

Final Words

Credit offers opportunity but requires discipline, while debit ensures safety but limits flexibility. Both are essential tools when used wisely.

Conclusion:

Understanding the difference between credit & debit is crucial in today’s financial world. While credit gives you the power to borrow and build financial history, debit keeps your spending grounded and secure. Each has its strengths and weaknesses, and the best choice depends on your financial goals and habits.

By learning how to use both effectively, you can avoid unnecessary debt, manage your money better, and achieve financial stability. Ultimately, mastering the difference between credit & debit empowers you to make smarter financial decisions and live a more balanced life.

I am an English content writer with more than 8 years of experience in writing about English word differences, grammar clarity, and everyday language usage. I am passionate about helping learners avoid common mistakes caused by similar-looking or confusing English words.

At diffruli.com, I write easy-to-understand guides that explain the difference between commonly confused words, spelling variations, and correct usage with real-life examples. My content is especially useful for students, writers, and non-native English speakers who want quick, accurate, and practical answers.